Car insurance for auto loan ensures protection and peace of mind when financing a vehicle. Understanding the nuances of this coverage is crucial for every car owner.

Exploring the various types of car insurance coverage, factors influencing insurance rates, and cost-saving tips can help individuals make informed decisions about their auto loans.

Understanding Car Insurance for Auto Loan

When you take out an auto loan to finance the purchase of a vehicle, it is essential to understand the role of car insurance in this process. Car insurance is a type of coverage that protects you financially in case of accidents, theft, or damage to your vehicle. In the context of auto loans, car insurance plays a crucial role as it provides a layer of protection for both you and the lender.

How Car Insurance Works in the Context of Auto Loans

Car insurance works by providing coverage for your vehicle in exchange for regular premium payments. When you have an auto loan, the lender will typically require you to have comprehensive and collision coverage to protect their investment in case of an accident. This means that if your car is damaged or totaled, the insurance will help cover the costs, ensuring that you can continue making payments on the loan.

The Importance of Having Car Insurance When Taking Out an Auto Loan

Having car insurance is crucial when taking out an auto loan because it protects both you and the lender from financial loss. In the event of an accident, theft, or damage to your vehicle, car insurance can help cover the costs of repairs or replacements, ensuring that you are not left with a significant financial burden. Additionally, having the right insurance coverage can give you peace of mind knowing that you are protected in case of unforeseen circumstances.

Types of Car Insurance Coverage

Car insurance coverage is an essential component when obtaining an auto loan. There are several types of car insurance coverage available that cater to different needs and situations. Understanding the differences between comprehensive, collision, liability coverage, and other specialized options like gap insurance is crucial for protecting your vehicle and financial investment.

Comprehensive Coverage

Comprehensive coverage provides protection in case of non-collision incidents such as theft, vandalism, natural disasters, or hitting an animal. This type of coverage helps repair or replace your vehicle if it is damaged or stolen.

Collision Coverage

Collision coverage is designed to cover damages to your vehicle resulting from a collision with another vehicle or object. This type of coverage is important for repairing or replacing your car in case of an accident.

Liability Coverage

Liability coverage is mandatory in most states and covers damages and injuries you are legally responsible for in an accident. This type of coverage helps pay for the other party’s medical bills, vehicle repairs, and legal fees.

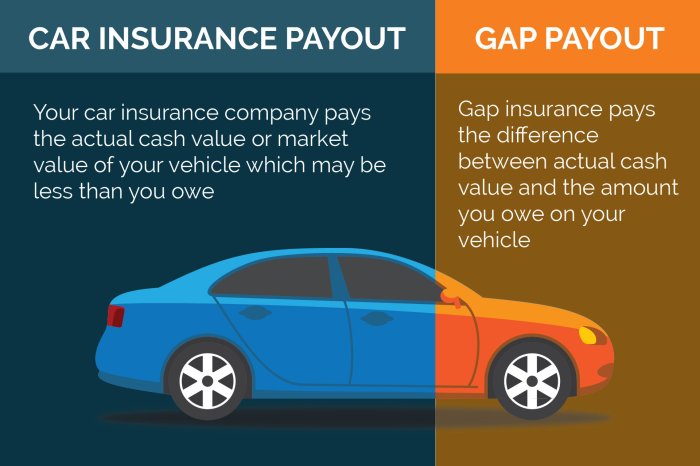

Gap Insurance

Gap insurance is an optional coverage that covers the difference between the actual cash value of your vehicle and the amount you owe on your auto loan in case of a total loss. This type of insurance ensures you are not left with a financial gap if your car is totaled.

Factors Influencing Car Insurance Rates for Auto Loans: Car Insurance For Auto Loan

When financing a vehicle, several factors come into play that can influence car insurance rates. Understanding these factors is crucial for individuals looking to secure the best insurance coverage at the most competitive rates.

Type of Vehicle

The type of vehicle being insured is a significant factor in determining insurance rates for auto loans. Generally, expensive or high-performance vehicles will have higher insurance premiums due to the increased cost of repair or replacement in the event of an accident.

Driving History

A driver’s history plays a crucial role in determining car insurance rates. Individuals with a history of accidents or traffic violations are considered higher risk and may face higher premiums. On the other hand, drivers with a clean record are likely to receive lower insurance rates.

Credit Score, Car insurance for auto loan

Credit score is another important factor that insurance companies consider when calculating rates for auto loans. A higher credit score generally indicates financial responsibility, leading to lower insurance premiums. Conversely, individuals with lower credit scores may face higher insurance costs.

Location and Usage of the Vehicle

The location where the vehicle is primarily kept and the frequency of use also impact insurance rates. Vehicles parked in urban areas with high crime rates may have higher premiums due to increased risk of theft or vandalism. Additionally, vehicles used for long commutes or business purposes may also result in higher insurance costs.

Tips for Saving on Car Insurance for Auto Loans

When financing a vehicle, car insurance can be a significant expense. However, there are strategies you can use to save on car insurance premiums for auto loans. By taking advantage of bundling options, discounts, and maintaining a good driving record, you can lower your insurance costs and make your auto loan more affordable.

Bundle Your Policies

One of the most effective ways to save on car insurance for auto loans is to bundle your policies. Many insurance companies offer discounts for customers who bundle their auto insurance with other policies, such as homeowners or renters insurance. By bundling your policies, you can save money on both your car insurance premiums and other insurance costs.

Take Advantage of Discounts

Insurance companies offer a variety of discounts that can help you save on car insurance for auto loans. These discounts may include safe driver discounts, good student discounts, multi-car discounts, and more. By asking your insurance provider about available discounts and taking advantage of them, you can reduce your insurance costs significantly.

Maintain a Good Driving Record

One of the most important factors that influence car insurance rates for auto loans is your driving record. By maintaining a good driving record and avoiding accidents and traffic violations, you can lower your insurance expenses. Safe drivers are often rewarded with lower premiums, so it’s essential to drive responsibly to save on car insurance costs.

Increase Your Deductible

Another way to save on car insurance for auto loans is to increase your deductible. By choosing a higher deductible, you can lower your insurance premiums. Keep in mind that you’ll need to pay more out of pocket in the event of a claim, so make sure you can afford the higher deductible before making this decision.

Shop Around for the Best Rates

Finally, to save on car insurance for auto loans, it’s essential to shop around for the best rates. Get quotes from multiple insurance providers and compare coverage options and premiums. By exploring different insurance companies, you can find the best deal that meets your coverage needs and budget.

In conclusion, securing the right car insurance for an auto loan is a smart financial move that can safeguard you from unexpected expenses. By considering the different coverage options and factors impacting insurance rates, you can make the best choices for your vehicle and budget.

Check what professionals state about Car insurance for cars with a clean record and its benefits for the industry.